Award-winning PDF software

Form 4876-A for Austin Texas: What You Should Know

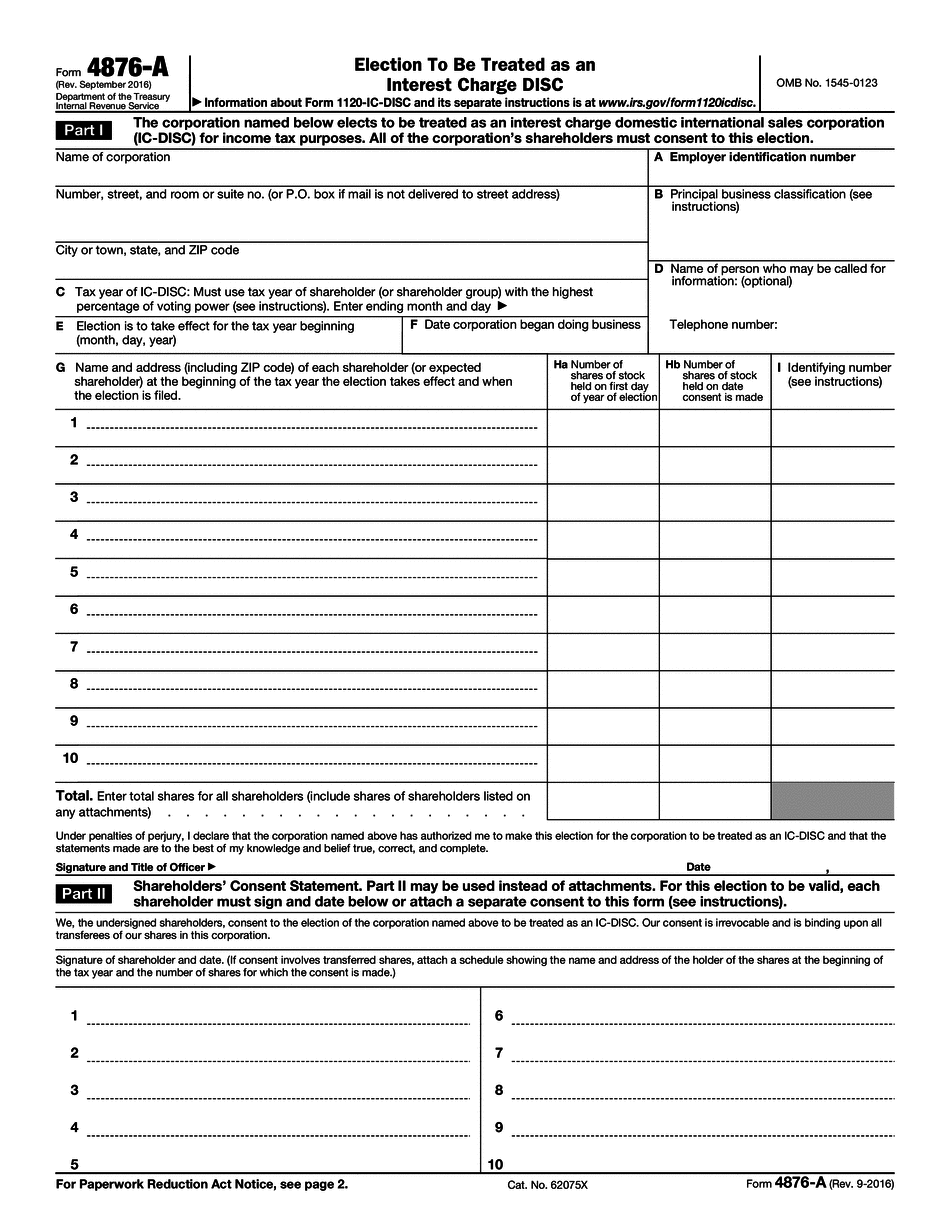

The corporation is not required to file or pay any federal tax, but is required to pay tax on some of its income. The corporate income tax rate in effect on the date the election is made is 14% or 25%. However, the tax on corporate income will continue to be 10%. If the individual is a U.S. citizen residing in the State of the foreign corporation's tax jurisdiction, the corporation shall be treated as owned by the individual, and may not be taxed on its foreign income. The corporation may sell or distribute income from its domestic source. If the corporation is sold or an interest, dividend or other return of capital is distributed by the corporation to a foreign entity, or any interest, dividend, or other return of capital from such a sale, distribution or distribution to the stockholders of such foreign entity, the corporation shall pay to the foreign entity the amount of such distribution or interest. If the corporation becomes an IC-DISC, the corporation may elect to be treated as an IC-DISC by filing Form 4876-A. An amendment making the election and certifying that the election has been properly made and accepted must also be filed with the Secretary. A corporation that does not elect to be treated as an interest rate corporation and has a taxable income of 3,000,000 or less may be treated as a rate corporation under the income tax laws of any foreign country with which the U.S. has a tax treaty. If a foreign country with which the U.S. has a tax treaty has a special rate of tax for a rate period (such as the tax rate applicable for income from real property held in a foreign country under U.S. law), the United States may deduct the amount of such special rate for a corporation with taxable income, up to the amount of the special rate for such corporation. An entity which qualifies as a rate corporation under U.S. law is not considered foreign for the purpose of applying the provisions of sections 901 (other than subsections (b) and (c) of section 901), 9003 (other than section 9031(a) of the Internal Revenue Code of 1986) and 9031(b) of such Code on the entity. For the purposes of subsections (a), (b), (c), and (d) of section 902, a rate corporation of which the shareholders of record do not elect to be treated as foreign under U.S.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 4876-A for Austin Texas, keep away from glitches and furnish it inside a timely method:

How to complete a Form 4876-A for Austin Texas?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 4876-A for Austin Texas aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 4876-A for Austin Texas from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.