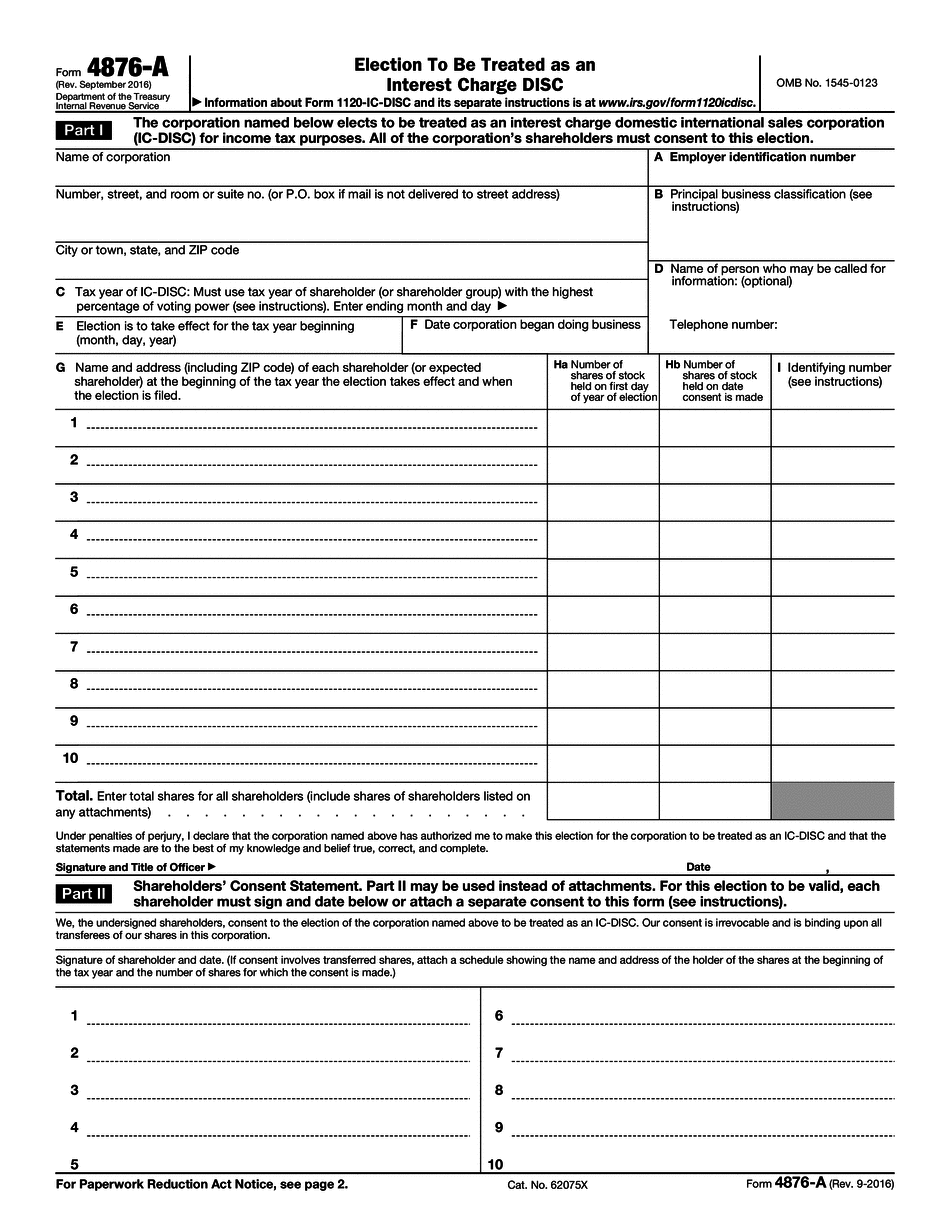

Creating your own Form 4876-A can be a straightforward process if you have the necessary information and follow the guidelines. Here is some relevant content to help you understand and create Form 4876-A:

1. What is Form 4876-A?

Form 4876-A, also known as the Projected Annual Accounting (PAA) form, is used by individuals or businesses engaged in farming activities to calculate their projected income, expenses, and deductions for the upcoming tax year. It helps estimate their tax liability and ensures accurate payments to the Internal Revenue Service (IRS).

2. Understanding the Purpose of Form 4876-A:

Form 4876-A is filed by taxpayers who have irregular income streams due to farming activities. This form helps them avoid underpayment penalties by ensuring they pay enough estimated taxes throughout the year.

3. Gathering Information:

Before creating Form 4876-A, gather the necessary information such as previous year's tax return, farming income records, expenses, anticipated future income, expected deductions, and any other relevant financial documents.

4. Creating your Own Form 4876-A:

To create your own Form 4876-A, follow these steps:

a. Begin by providing your name, Social Security number (SSN), EIN (if applicable), and address on the top section of the form.

b. Proceed to Part I - Farm Income. Document your projected income from farming activities, including crops, livestock, government program payments, sales of livestock, produce, or any other income sources related to your farm activities.

c. Move on to Part II - Farm Expenses. List all projected expenses related to your farming activities, such as costs for seeds, fertilizers, feed, veterinary expenses, farm equipment, hired labor, insurance premiums, property taxes, and any other relevant expenses.

d. Next, complete Part III - Depreciation and Amortization. Provide details of any depreciation or amortization deductions for farm-related assets, such as machinery, breeding livestock, buildings, land improvements, or other depreciable assets.

e. Proceed to Part IV - Farm Deductions. Document any additional deductions that are applicable to your farming activities, such as business use of a personal vehicle, home office deduction, or other relevant deductions.

f. Once you have completed the appropriate sections, calculate your projected taxable income and tax liability using the provided schedules, tables, and formulas on the form. Pay close attention to any specific instructions provided by the IRS.

g. Lastly, sign and date the form where indicated, certifying that the information provided in Form 4876-A is true, accurate, and complete to the best of your knowledge.

5. Seeking Guidance or Professional Help:

If you are uncertain about creating your own Form 4876-A or need assistance in determining your projected income and expenses accurately, consider consulting a tax professional or utilizing tax software that specializes in farm tax reporting.

Remember to keep a copy of the completed Form 4876-A for your records and consult the IRS guidelines or seek professional advice to ensure compliance with any updates or changes to tax regulations.